2026 State of Merchant Onboarding is out

Get the Report

Ballerine is a YC-backed open-source risk infrastructure platform with a strong KYC/KYB orchestration layer. Engineering teams that want flexible, configurable verification workflows can self-host it and build custom flows with third-party data providers. In the broader fintech space, Ballerine has earned its position as a credible risk-orchestration option.

Ballerine is horizontal risk infrastructure. It was designed for the generic fintech use case, where the compliance layer is the heaviest workflow. For ISOs, PayFacs, and acquirers, compliance is one stage out of five. The merchant lifecycle starts before the compliance check and continues long after it.

Ballerine doesn't analyze merchant statements. It doesn't generate branded merchant applications. It doesn't board merchants to processors via API. It doesn't monitor portfolio pricing for revenue leakage. These aren't features Ballerine chose to skip — they're outside its scope because payments isn't its market.

For payments companies, the gap between "compliance orchestration" and "merchant lifecycle platform" is four full operational stages. That's the gap this page is about.

See how Gratify's payments-native lifecycle stacks up against Ballerine's horizontal risk orchestration.

Your rep uploads a merchant statement. Gratify returns a margin analysis and branded quote in 60 seconds. The pre-compliance stage is the entire reason your sales motion accelerates — and it's where Ballerine has no answer.

Twenty to forty-five minutes of manual statement review collapses into the time it takes to send a follow-up email. Your reps win deals on accurate pricing instead of estimates.

The analysis pulls processor fees, surcharges, and ancillary line items into a single branded view per ISO. The merchant sees pricing they can act on, not a generic pitch.

Ballerine's KYC/KYB orchestration runs after the application is filled out. Statement Analyzer runs before it opens.

Ballerine doesn't touch this stage. It's the gap between fintech compliance and a payments sales motion.

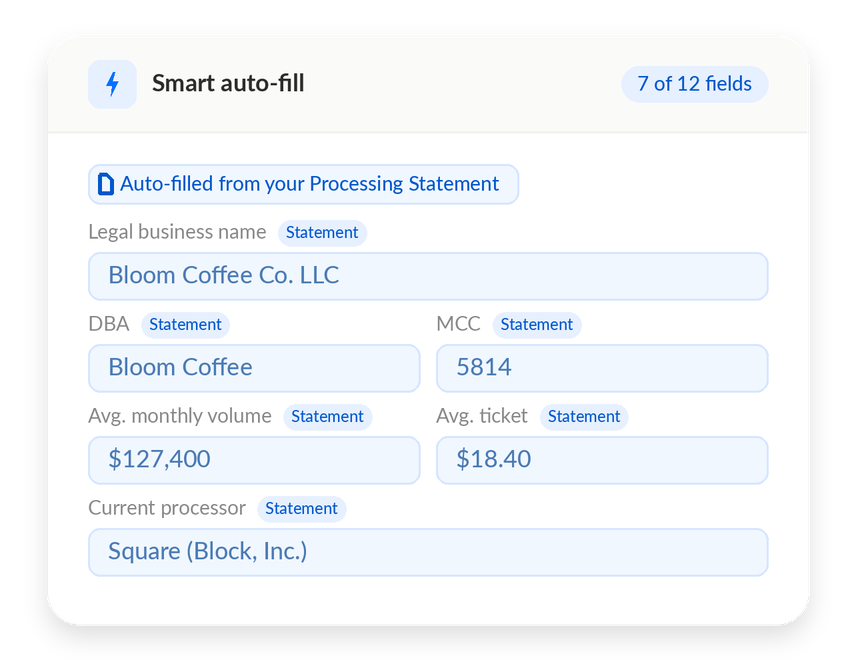

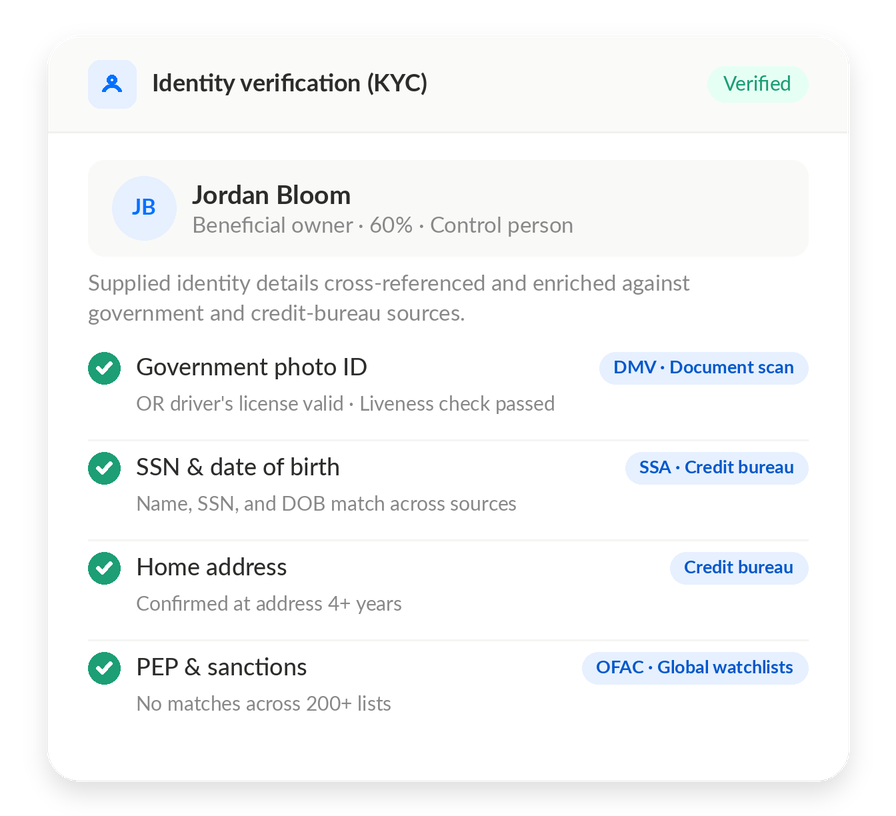

Each ISO gets a branded subdomain for merchant applications. The merchant fills out one form. KYC/KYB verification, OFAC sanctions, BBB lookup, prohibited MCC validation, and eSignature all run automatically inside the same flow.

Ballerine handles KYC/KYB orchestration as a separate layer. Gratify wraps that verification inside the branded application your sales team sends to merchants — with daily PEP and sanctions rescreening on the back end.

The merchant doesn't see a compliance UX bolted onto an application. They see one branded form that knows what it needs. Your underwriting team doesn't re-enter merchant data from a separate verification system.

Ballerine + your own application platform requires integration work. Gratify ships with the branded application platform built in, with verification embedded by default.

Daily PEP and sanctions rescreening continues after onboarding.

Compliance is a continuous stage in the merchant's life, not a one-time gate.

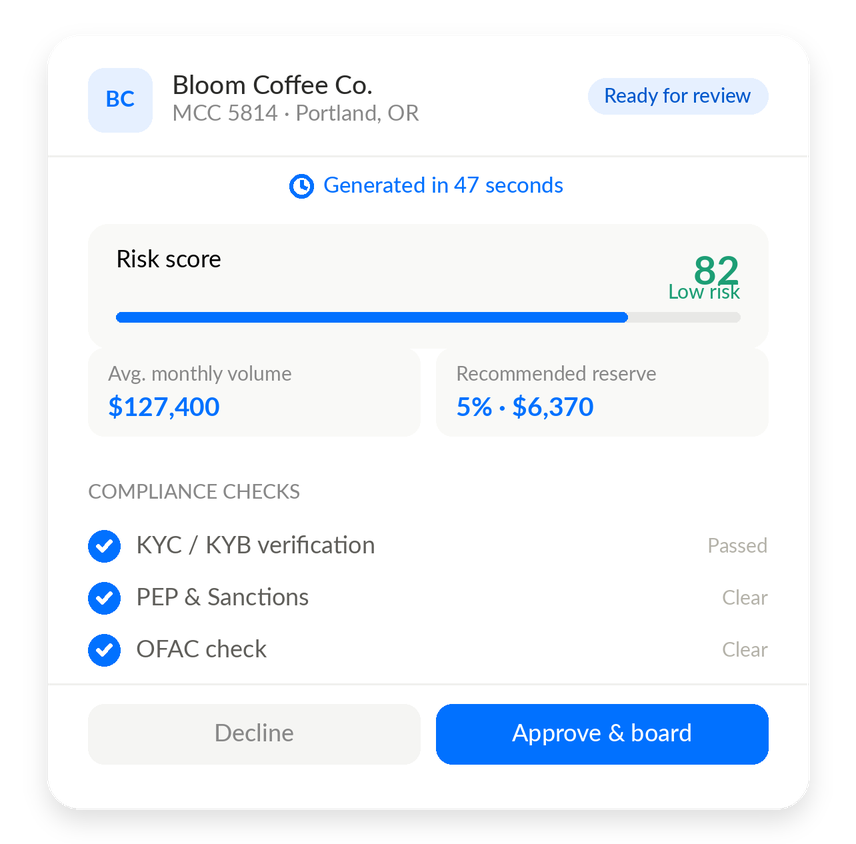

62+ configurable data points across three risk categories. Letter-grade scoring (A/B/C/D) with reserve recommendations. 1,627 MCC codes with chargeback ratios. ISO-configurable rules. Ballerine orchestrates compliance workflows; Gratify produces an underwriting decision.

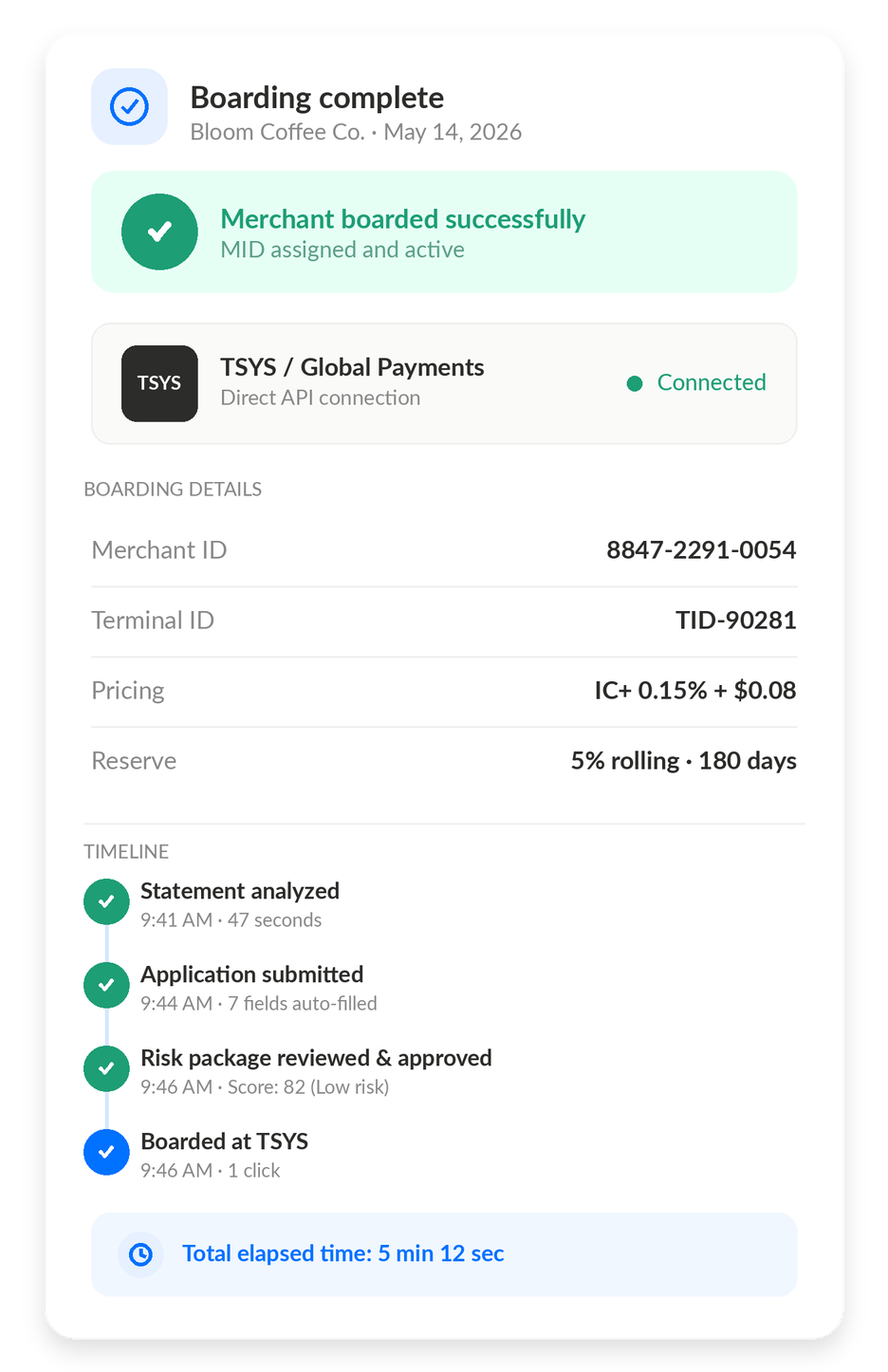

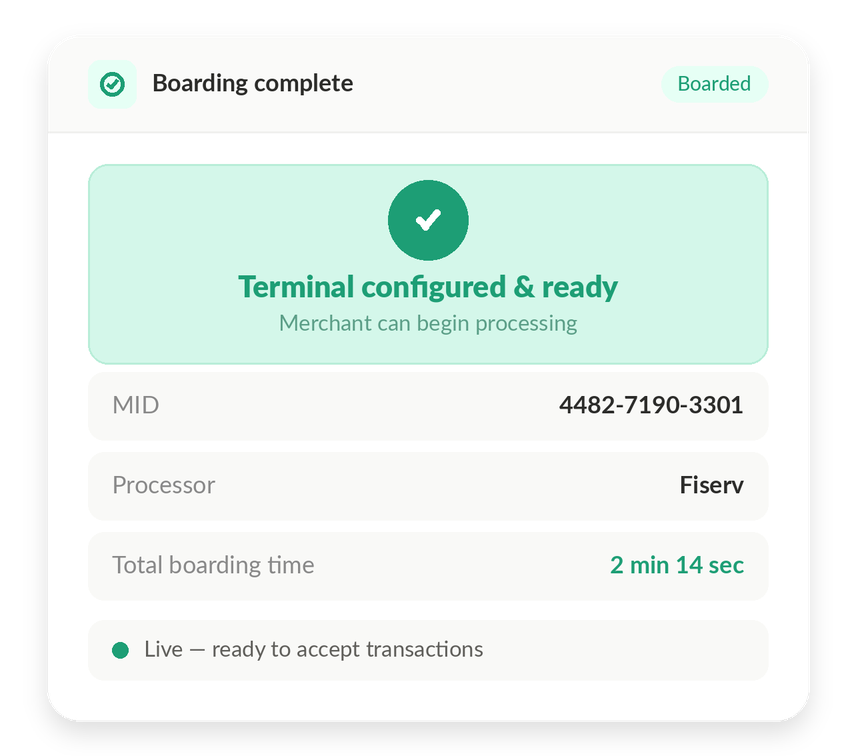

Direct API boarding to TSYS, Dejavoo, Repay, and Fiserv. One click from approved merchant to live processor. Ballerine isn't an onboarding platform — it has no processor integrations. This is the stage where the lifecycle leaves the compliance layer entirely.

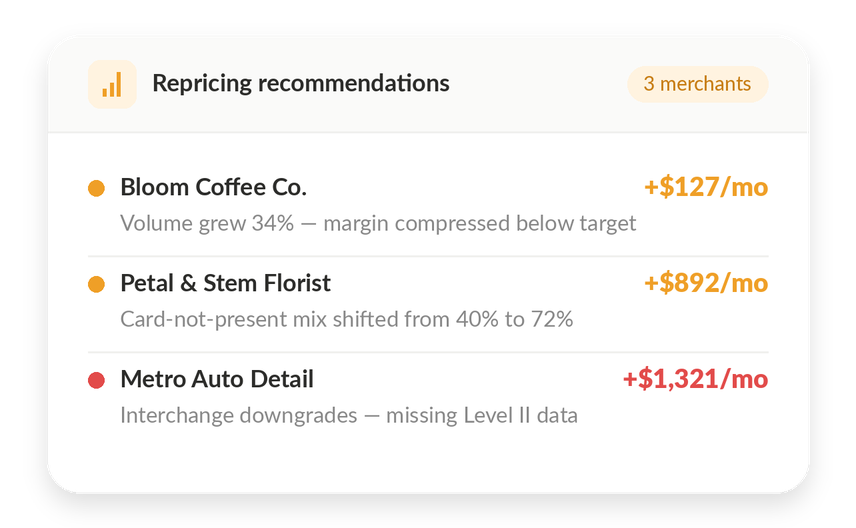

Daily monitoring of total volume, active merchant count, average markup BPS, and average effective rate. Before/after comparison on every reprice. Ballerine ends at compliance; Gratify protects the portfolio for the merchant's full life on book.